Medicare 101 Beginner's Guide: Latest Changes and Key Underwriting Points for 2026–2027

- Ivy Yang

- 8 hours ago

- 11 min read

Last Updated: 07/16/2026

Does receiving a Medicare card mean all your medical expenses will be paid? Not necessarily.

"Red and Blue Card" usually refers to Part A and Part B of Original Medicare. It is the core of Medicare, but it does not necessarily include routine prescription medications and does not have the usual annual deductible. Dental care, vision care, hearing aids, and overseas medical treatment may not be fully covered.

For Medicare newbies, the real task isn't just asking "which plan is best," but rather figuring out:

1. When is it necessary to apply?

2. What are the responsibilities of each of Parts A, B, C, and D?

3. Should I choose Original Medicare with Medigap, or Medicare Advantage?

4. Which route best suits your doctor, medications, budget, and travel needs?

Let me explain step by step.

🩺 What is Medicare? Who can apply?

Medicare is a federal health insurance company in the United States. Its main services include:

- Eligible individuals must be 65 years of age or older;

- Individuals under 65 years of age who meet specific disability qualifications;

- Individuals who meet the criteria and have end-stage renal disease (ESRD) or ALS.

Medicare and Medicaid are different. Medicare eligibility is primarily determined by age, employment history, or specific health qualifications; Medicaid eligibility is primarily determined by income, assets, and state regulations. Some people can have both, a condition known as dual eligibility (Medicare-Medicaid).

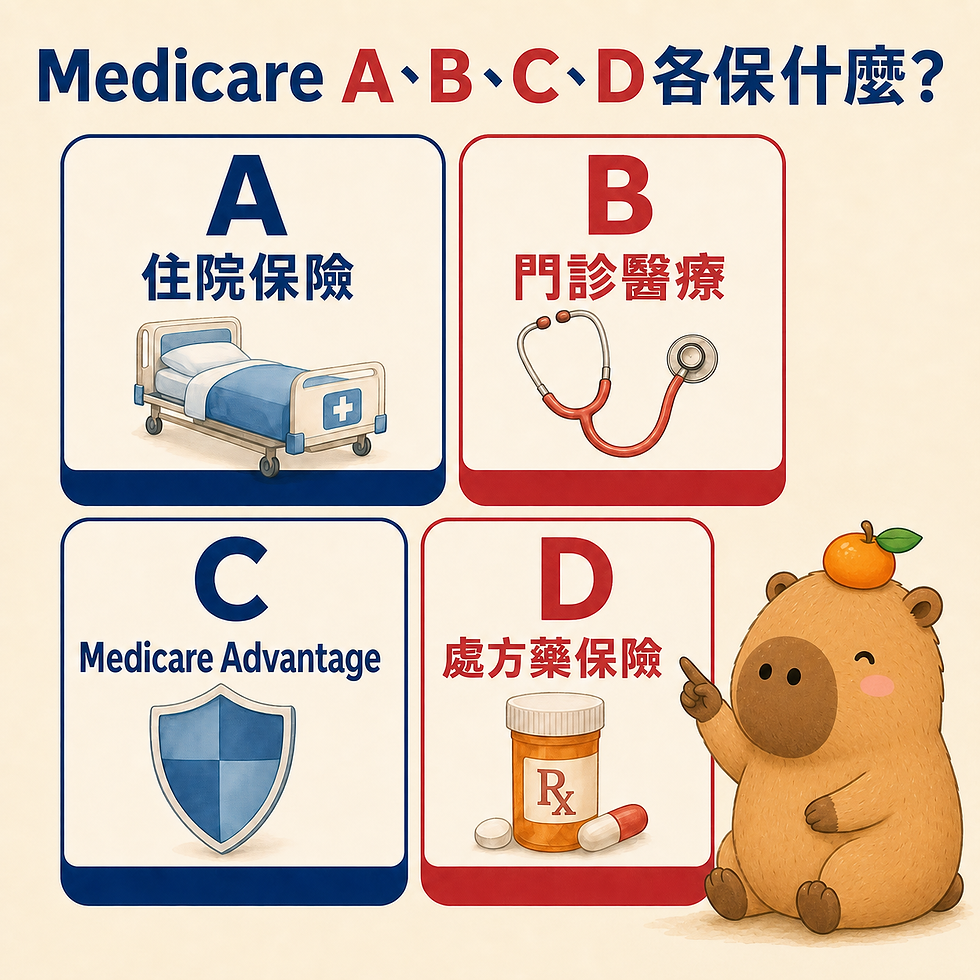

🧩 Parts A, B, C, and D, understand them all at once

🏥 Part A: Hospitalization Insurance

It mainly covers inpatient care, care in qualified professional nursing institutions, palliative care, and some home-based medical care.

Most individuals or their spouses who have accumulated at least 40 working quarters, or approximately 10 years, of Medicare tax records are exempt from paying Part A monthly premiums. However, "premium waiver" does not equate to free hospitalization; deductibles and daily co-insurance may still apply.

🩺 Part B: Outpatient Services and Medical Insurance

It mainly covers doctor consultations, outpatient services, preventive healthcare, durable medical equipment, and some home healthcare.

Part B typically includes a monthly premium and an annual deductible. Once the deductible is reached, Medicare covers 80% of most Medicare-approved services, with the individual usually paying 20%. High-income earners may also pay an IRMAA income bonus.

🛡️ Part C: Medicare Advantage

Medicare Advantage (MA) is a plan offered by Medicare-approved private insurance companies as a primary payment alternative to Original Medicare. Part A and Part B must be in place before enrolling.

MA plans must cover Original Medicare services, most also include Part D prescription drugs, and may provide dental, vision, hearing, fitness or other additional benefits.

However, plans usually include provisions for healthcare networks, service areas, referrals, or prior authorization. A "$0 monthly premium" label does not mean it's completely free, as a Part B monthly premium is still required, and there may be copays for medical visits, deductibles, and an annual maximum deductible.

💊 Part D: Prescription Drug Insurance

Part D is provided by a private insurance company and helps cover outpatient prescription drug costs. The drug formulary, drug class, pharmacy network, and prices may vary for each plan.

Even if you don't currently have a regular medication, you shouldn't skip Part D. If you miss Part D for 63 consecutive days or more without creditable drug coverage, you may be required to pay late addition penalties in the future.

📅 The most important first step: Don't miss the application deadline.

For most people, the Initial Enrollment Period (IEP) lasts for 7 months.

- The three months preceding your 65th birthday;

- The month of one's birthday;

- 3 months after your birth month.

If your birthday is on the 1st of each month, the time calculation will be done one month earlier.

People who are already receiving Social Security or Railroad Retirement Board benefits may be automatically enrolled in Part A and Part B; others usually need to apply proactively.

Being employed and having employer-sponsored group insurance does not guarantee a safe postponement of Part B. Whether a postponement is possible typically depends on whether the insurance is based on "your or your spouse's current employment," the size of the employer, and whether the insurance company is a primary payer for Medicare. COBRA, Retirement Insurance, or Marketplace Insurance are generally not considered equivalent to employed group insurance.

Missing the right time may create a coverage gap and result in Part A, Part B, or Part D late payment penalties. Part B penalties typically increase by 10% for each full 12-month delay, and in most cases, they will be paid over a long period along with the Part B premium.

🍊 Little Capybara reminds you: When you are about to turn 65, it is best to start planning your retirement date and current insurance 3 to 6 months in advance, rather than waiting until your birthday month.

🛤️ After obtaining a Medicare card, there are two common insurance routes.

🔵 Route 1: Original Medicare + Part D + Medigap

This road typically includes:

- Original Medicare Part A + Part B;

- Independent Part D prescription regimen;

- Optional Medicare Supplement Insurance (Medigap) can be purchased to help cover part of the deductible, co-insurance, and copay.

May be suitable for:

- To have access to any doctor or hospital across the United States that accepts Medicare;

- Frequently resides or travels across state lines;

- Hoping to reduce fluctuations in medical costs;

- Willing to pay higher, but relatively predictable, monthly premiums.

Original Medicare does not have an annual maximum deductible. Medigap reduces this risk, but premiums vary depending on location, age, company, and plan. Medigap is not the same as Part D; Medigap policies issued after 2006 generally do not include prescription drug coverage.

The crucial Medigap application period typically begins six months after you reach age 65 and Part B is in effect. During this federal Medigap Open Enrollment Period, you usually enjoy more comprehensive coverage. If you change or reapply later, unless you meet the guaranteed coverage requirements or are otherwise protected by state law, the insurance company may conduct health underwriting, increase premiums, or refuse coverage.

🔴 Route Two: Medicare Advantage (Part C)

This route integrates Part A and Part B in private insurance plans, and most plans also include Part D.

May be suitable for:

- Prefers to integrate medical and drug coverage into a single plan;

- Commonly used doctors, hospitals, and medications are all included in the program's network and medication list;

- Emphasis is placed on additional benefits such as dental care, vision, and hearing;

- Acceptable network, referral and prior authorization requirements.

MA plans have an annual maximum deductible, but the amount and calculation method vary from plan to plan. When choosing a plan, you should not only look at the extra benefits or $0 monthly premium, but also check the family doctor, specialist doctor, hospital, pharmacy and commonly used pharmacies.

Medigap cannot be used to pay for Medicare Advantage copays, co-insurance, or deductibles; generally, Medigap and Medicare Advantage cannot be used simultaneously.

🍊 Capybara Tip: Don't just compare monthly premiums; doctor networks, medication lists, and the maximum annual out-of-pocket risk are equally important.

💰 2026 Medicare Costs Highlights

The following are the federal standard amounts for 2026:

Part A out-of-pocket expenses for hospitalization are calculated on a benefit period basis, not paid only once a year. The actual costs for Part B and Part D may also be affected by income boosting, the chosen treatment plan, medication use, and service usage.

✨ New changes that took effect in 2026

💊 1. The annual deductible for Part D has been adjusted to $2,100.

In 2026, the annual out-of-pocket cost cap for prescription drugs that meet the Part D calculation rules will be $2,100. Once this cap is reached, cost sharing will generally not be paid for Part D covered drugs for the remainder of the year.

The Medicare Prescription Payment Plan helps manage cash flow by spreading out-of-pocket expenses for prescription drugs over the remaining months of the year; however, it does not reduce drug prices or the total annual cost.

💵 2. Prices for the first batch of 10 Medicare negotiated drugs take effect

The negotiated prices for the first 10 Part D drugs under the Medicare drug price negotiation program took effect on January 1, 2026. The actual savings will depend on the chosen program, the drug list, supply, and the pharmacy.

🩻 3. Added CT colonography screening

In 2026, Medicare will add coverage for eligible CT colonography colorectal cancer screenings. The frequency varies depending on whether the risk level is high; if the physician is on Medicare assignment, eligible screenings will be free of charge.

🌉 4. GLP-1 Bridge was commissioned in July 2026.

Starting July 1, 2026, eligible beneficiaries enrolled in Part D will be able to access certain GLP-1 weight management medications through the Medicare GLP-1 Bridge for a monthly copay of $50. The program is currently scheduled to run until December 31, 2027.

This is a demonstration program that operates independently of the standard Part D benefit process and requires eligibility and prior authorization. The $50 copay is not included in the annual out-of-pocket expenses for Part D, and the low-income allowance will not reduce this copay.

🔭 What changes have been finalized for 2027?

As of July 2026, CMS has released the 2027 Medicare Advantage and Part D Final Rules, but the 2027 Part A/Part B premiums, deductibles, annual Part D caps, and individual MA/Part D plan premiums and benefits in various regions have not yet been fully disclosed. These amounts are usually confirmed gradually as the 2027 policy-buying season approaches.

The areas that have already been finalized and are of particular interest to general beneficiaries include:

The new Part D framework continues and is formally incorporated, including the elimination of the previous coverage gap stage, a reduction in the annual out-of-pocket threshold, and the cessation of cost sharing charges after entering the catastrophic phase;

The Medicare Advantage and Part D star ratings have been updated, and some administrative indicators that could not effectively differentiate the performance of the plan have been removed.

A new quality measure related to depression screening and follow-up has been added, but this indicator will be reflected in the 2029 Star Ratings starting from the 2027 measurement year.

Simplify the administrative procedures for some parts of the plan;

The Medicare GLP-1 Bridge has been extended to December 31, 2027.

In other words, the policy direction for 2027 has been partially finalized, but how much individuals will actually pay, what plans are available in their locality, and how the physician network and drug list will change will still depend on the Annual Notice of Change (ANOC), Evidence of Coverage (EOC), and Medicare Plan Finder received in the fall of 2026.

🍊 Little Capybara Reminder: When you see "2027 Latest", first distinguish whether it is a finalized rule or policy direction, or an individual plan fee that has not yet been announced.

✅ 7 things to check before choosing a plan for beginners

Don't just compare monthly premiums. Please prepare the following information:

1. 👩⚕️ Doctors and Hospitals: Do family doctors, specialists, and preferred hospitals accept Medicare or are they within the MA network?

2. 💊 Complete prescription: Have the medication name, dosage, frequency of use, and preferred pharmacy been entered and compared?

3. 🧮 Total annual cost: In addition to premium, you also need to look at deductible, copay, coinsurance and maximum out-of-pocket expenses.

4. 🧳 Travel and Residence Habits: Do you live across states, travel frequently, or require overseas emergency medical coverage?

5. 🎁 Additional benefits restrictions: Are there any network access and conditions for dental allowances, glasses, hearing aids, transportation, or OTC benefits?

6. 📋 Prior Authorization: Do commonly used treatments, examinations, medical equipment, or medications require prior authorization?

7. 🔄 Future convertibility: If I choose MA now, will I be able to successfully obtain Mediigap when I return to Original Medicare in the future?

🔔 Annual inspection is necessary; don't let automatic renewal leave you unattended.

The premiums, drug list, medical network, copay, and benefits for Medicare Advantage and Part D plans may change annually.

The Medicare Open Enrollment Period runs from October 15 to December 7 each year. During this period, you can compare and make changes to the plan for the following year, with most changes taking effect on January 1 of the following year.

Those already enrolled in Medicare Advantage have an additional Medicare Advantage Open Enrollment Period from January 1 to March 31 each year, during which they can switch to another Medicare plan or return to Original Medicare and enroll in Part D; however, they generally cannot enroll in a new Medicare plan from Original Medicare during this period.

🌟 Conclusion: First consider your living needs, then look at the plan name.

There is no single best answer for everyone when it comes to Medicare.

Before making a choice, consider your doctor, prescription medications, budget, travel habits, chronic disease management, and risk tolerance. A low monthly premium does not necessarily mean the cheapest option for the whole year; many benefits do not necessarily mean the most suitable one.

If you are approaching 65, it is recommended that you start preparing your retirement date, employer insurance, doctor and medication information at least 3 to 6 months in advance. The earlier you start, the more you can avoid coverage gaps, late payment penalties, and the difficulty of switching Medigap later.

💬 Need one-on-one assistance?

If you are unsure whether to choose Original Medicare, Medigap, Part D, or Medicare Advantage, you can prepare the following information for a personalized comparison:

- Postal code;

- Effective date of Medicare Part A/Part B;

- Complete list of prescription drugs;

- Commonly used doctors and hospitals;

- Current employer, retirement, or other health insurance;

- Monthly budget and travel needs.

❓ III. Frequently Asked Questions (FAQ)

1. Is Medicare a full form of insurance?

No. The red and blue card usually stands for Original Medicare Part A and Part B. It generally doesn't include routine outpatient prescriptions and doesn't have an annual maximum out-of-pocket expense. You may also need Part D, Medigap, or choose Medicare Advantage.

2. Does Part A being free mean that hospitalization is free?

No. Most people do not need to pay the monthly premium for Part A, but may still be able to pay the deductible for each benefit period when hospitalized, as well as daily co-insurance during longer hospital stays.

3. Is Medicare Advantage's $0 monthly premium truly free?

No. $0 usually only means that the MA plan itself does not have an additional monthly premium. You still need to pay the Part B premium and pay copay, coinsurance, or deductible based on the services you use.

4. Can Medicare Advantage be used in conjunction with Medigap?

Medigap cannot be used to pay for Medicare Advantage deductibles. These are different coverage lines and typically cannot be used simultaneously.

5. I am still working, can I not apply for Part B?

It's possible, but you must first confirm whether your current insurance comes from your or your spouse's "working" employer group plan, the size of the employer, and the payment order. COBRA and retirement insurance are not usually the same as working group coverage.

6. Do I need Part D even if I'm not taking any medication?

If there is no other creditable drug coverage, delaying Part D for more than 63 days may result in long-term penalties. Lower-premium plans may be considered, but should still be compared based on location and individual circumstances.

7. What is the maximum out-of-pocket expense for Part D prescription drugs in 2026?

The target is $2,100 in 2026, applicable to out-of-pocket expenses for prescription drugs covered by Part D and accounted for according to the rules. Once this target is reached, cost-sharing for Part D covered drugs is generally no longer payable for the remainder of the year.

8. Have the 2027 Medicare premiums been released yet?

As of July 2026, the full premiums and deductibles for Part A and Part B in 2027, as well as individual plan prices in different regions, have not yet been fully released. Please check CMS, Medicare.gov, and the ANOC plan again in the fall of 2026.

This content is for general educational and informational purposes only and does not constitute medical, legal, tax, or specific insurance plan advice. Medicare rules, premiums, benefits, healthcare networks, drug lists, and plan availability are subject to change and vary depending on location and individual eligibility. Please refer to the latest documents from Medicare.gov, CMS, Social Security, state governments, and individual insurance plans. Contacting an insurance agent does not affect your obligation or right to enroll in Medicare.

Further reading:

- [Medicare.gov: 2026 Medicare Costs](https://www.medicare.gov/basics/get-started-with-medicare/medicare-basics/what-does-medicare-cost)

- [CMS: 2026 Medicare Part A/B Premiums and Deductibles](https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles)

- [Medicare.gov: Part D Costs and 2026 Out-of-Pocket Limits](https://www.medicare.gov/health-drug-plans/part-d/basics/costs)

- [Medicare.gov: Latest Changes in 2026](https://www.medicare.gov/publications/12229-your-medicare-in-2026-what-you-need-to-know.pdf)

- [Medicare.gov: Initial Application Period and Effective Date](https://www.medicare.gov/basics/get-started-with-medicare/sign-up/when-does-medicare-coverage-start)

- [Medicare.gov: Comparison of Original Medicare and Medicare Advantage](https://www.medicare.gov/basics/get-started-with-medicare/get-more-coverage/your-coverage-options/compare-original-medicare-medicare-advantage)

- [Medicare.gov: Medigap Basic Rules](https://www.medicare.gov/health-drug-plans/medigap/basics/how-medigap-works)

- [CMS: 2027 Medicare Advantage and Part D Final Rule](https://www.cms.gov/newsroom/fact-sheets/contract-year-2027-medicare-advantage-part-d-final-rule)

- [CMS: Medicare GLP-1 Bridge](https://www.cms.gov/medicare/coverage/prescription-drug-coverage/medicare-glp-1-bridge)

Comments